Free Preparation Discussions

Free CFA Institute CFA-Level-II Exam Dumps June 2026

Here you can find all the free questions related with CFA Institute CFA Level II Chartered Financial Analyst (CFA-Level-II) exam. You can also find on this page links to recently updated premium files with which you can practice for actual CFA Institute CFA Level II Chartered Financial Analyst Exam. These premium versions are provided as CFA-Level-II exam practice tests, both as desktop software and browser based application, you can use whatever suits your style. Feel free to try the CFA Level II Chartered Financial Analyst Exam premium files for free, Good luck with your CFA Institute CFA Level II Chartered Financial Analyst Exam.MultipleChoice

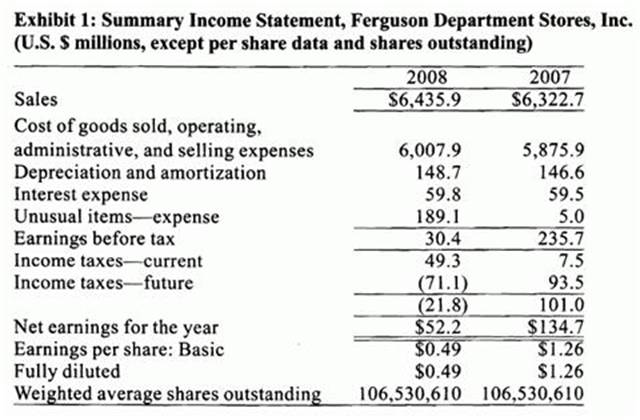

Matthew Emery, CFA, is responsible for analyzing companies in the retail industry. He is currently reviewing the status of Ferguson Department Stores, Inc. (FDS). FDS has recently gone through extensive restructuring in the wake of a slowdown in the economy that has made retailing particularly challenging. As part of his analysis, Emery has gathered information from a number of sources.

Ferguson Department Stores, Inc.

FDS went public in 1969 following a major acquisition, and the Ferguson name quickly became one of the most recognized in retailing. Ferguson had been successful through most of its first 30 years in business and has prided itself on being the one-stop shopping destination for consumers living on the West Coast of the United States. Recently, FDS began to experience both top and bottom line difficulties due to increased competition from specialty retailers who could operate more efficiently and offer a wider range of products in a focused retailing sector. When the company's main bank reduced FDS's line of credit, a serious working capital crisis ensued, and the company was forced to issue additional equity in an effort to overcome the problem. FDS has a cost of capital of 10% and a required rate of return on equity of 12%. Dividends are growing at a rate of 8%, but the growth rate is expected to decline linearly over the next six years to a long-term growth rate of 4%. The company recently paid an annual dividend of $1.

At the end of 2008, FDS announced that it would be expanding its retail operations, moving to a warehouse concept, and opening new stores around the country. FDS also announced it would close some existing stores, write-down assets, and take a large restructuring charge. Upon reviewing the prospects of the firm, Emery issued an earnings per share forecast for 2009 of $0.90. He set a 12-month share price target of $22.50. Immediately following the expansion announcement, the share price of FDS jumped from $14 to $18.

In 2008, FDS also reported an unusual expense of $189.1 million related to restructuring costs and asset write downs.

In response to questions from a colleague, Emery makes the following statements regarding the merits of earnings yield compared to the P/E ratio:

Statement 1: For ranking purposes, earnings yield may be useful whenever earnings are either negative or close to zero.

Statement 2: A high E/P implies the security is overpriced.

Assuming a tax rate of 34%, the underlying earnings per share (EPS) for FDS in 2008 is closest to:

OptionsMultipleChoice

William Bow, CFA, is a risk manager for GlobeCorp, an international conglomerate with operations in the technology, consumer products, and medical devices industries. Exactly one year ago, GlobeCorp, under Bow's advice, entered into a 3-year payer interest rate swap with semiannual floating rate payments based on the London interbank offered rate (LIBOR) and semiannual fixed rate payments based on an annual rate of 2.75%. At the time of initiation, the swap had a value of zero and the notional principal was set equal to $150 million. The counterparty to GlobeCorp's swap is NVS Bank, a commercial bank that also serves as a swap dealer. Exhibit 1 below summarizes the current LIBOR term structure.

Upper management at GlobeCorp feels that the original swap has served its intended purpose but that circumstances have changed and it is now time to offset the firm's exposure to the swap. Because they cannot find a counterparty to an offsetting swap transaction, management has asked Bow to come up with alternative measures to offset the swap exposure. Bow created a report for the management team which outlines several strategies to neutralize the swap exposure. Two of his strategies are included in Exhibit 2.

After examining its long-term liabilities, NVS Bank has decided that it currently needs to borrow $100 million over the next two years to finance its operations. For this type of funding need, NVS generally issues quarterly coupon short-term floating rate notes based on 90-day LIBOR. NVS is concerned, however, that interest rates may shift upward and the LIBOR curve may become upward sloping. To manage this risk, NVS is considering utilizing interest rate derivatives. Managers at the bank have collected quotes on over-the-counter interest rate caps and floors from a well known securities dealer. The quotes, which are based on a notional principal of $100 million, are provided in Exhibit 3.

One of the managers at NVS Bank, Lois Green, has expressed her distrust of the securities dealer quoting prices on the caps and floors. In a memo to the CFO, Green suggested that NVS use an alternative but equivalent approach to manage the interest rate risk associated with its two-year funding plan. Following is an excerpt from Green's memo:

"Rather than using a cap or floor, NVS Bank can effectively manage its exposure to interest rates resulting from the 2-year funding requirement by taking long positions in a series of put options on fixed-income instruments with expiration dates that coincide with the payment dates on the floating rate note."

"As a cheaper alternative, NVS can effectively manage its exposure to interest rates resulting from the 2-ycar funding requirement by creating a collar using long positions in a series of call options on interest rates and long positions in a series of call options on fixed income instruments all of which would have expiration dates that coincide with the payment dates on the floating rate note."

Determine which of the interest rate derivatives in Exhibit 3 is appropriate to manage the interest rate risk associated with NVS Bank's $100 million debt obligation and calculate the payoff from this derivative 360 days after the contract initiation if LIBOR at that time is expected to be 3.75%.

Options

MultipleChoice

Pat Wilson, CFA, is the chief compliance officer for Excess Investments, a global asset management and investment banking services company. Wilson is reviewing two investment reports written by Peter Holly, CFA, an analyst and portfolio manager who has worked for Excess for four years. Holly's first report under compliance review is a strong buy recommendation for BlueNote Inc., a musical instrument manufacturer. The report states that the buy recommendation is applicable for the next 6 to 12 months with an average level of risk and a sustainable price target of $24 for the entire time period. At the bottom of the report, an e-mail address is given for investors who wish to obtain a complete description of the firm's rating system. Among other reasons supporting the recommendation, Holly's report states that expected increases in profitability as well as increased supply chain efficiency provide compelling support for purchasing BlueNote.

Holly informs Wilson that he determined his conclusions primarily from an intensive review of BlueNote's filings with the SEC but also from a call to one of BlueNote's suppliers who informed Holly that their new inventory processing system would allow for more efficiency in supplying BlueNote with raw materials. Holly explains to Wilson that he is the only analyst covering BlueNote who is aware of this information and that he believes the new inventory processing system will allow BlueNote to reduce costs and increase overall profitability for several years to come.

Wilson must also review Holly's report on BigTirae Inc., a musical promotions and distribution company. In the report, Holly provides a very optimistic analysis of BigTime's fundamentals. The analysis supports a buy recommendation for the company. Wilson finds one problem with Holly's report on BigTime related to Holly's former business relationship with BigTime Inc. Two years before joining Excess, Holly worked as an investment banker and received 1,000 restricted shares of BigTime as a result of his participation in taking the company public. These facts are not disclosed in the report but are disclosed on Excess Investment's Web site. Wilson decides, however, that the timeliness of the information in the report warrants overlooking this issue so that the report can be distributed.

Just before the report is issued. Holly mentions to Wilson that BigTime unknowingly disclosed to him and a few other analysts who were wailing for a conference call to begin that the company is planning to restructure both its sales staff and sales strategy and may sell one of its poorly performing business units next year.

Three days after issuing his report on BigTime, which caused a substantial rise in the price of BigTime shares, Holly sells all of the BigTirne shares out of both his performance fee-based accounts and asset-based accounts and then proceeds to sell all of the BigTime shares out of his own account on the following day. Holly obtained approval from Wilson before making the trades.

Just after selling his shares in BigTime, Holly receives a call from the CEO of BlueNote who wants to see if Holly received the desk pen engraved with the BlueNote company logo that he sent last week and also to offer two front row tickets plus limousine service to a sold-out concert for a popular band that uses BlueNote's instruments. Holly confirms that the desk pen arrived and thanks the CEO for the gift and tells him that before he accepts the concert tickets, he will have to check his calendar to see if he will be able to attend. Holly declines the use of the limousine service should he decide to attend the concert.

After speaking with the CEO of BlucNote, Holly constructs a letter that he plans to send by e-mail to all of his clients and prospects with e-mail addresses and by regular mail to all of his clients and prospects without e-mail addresses. The letter details changes to an equity valuation model that Holly and several other analysts at Excess use to analyze potential investment recommendations. Holly's letter explains that the new model, which will be put into use next month, will utilize Monte Carlo simulations to create a distribution of stock values, a sharp contrast to the existing model which uses static valuations combined with sensitivity analysis. Relevant details of the new model are included in the letter, but similar details about the existing model are not included. The letter also explains that management at Excess has decided to exclude alcohol and tobacco company securities from the research coverage universe. Holly's letter concludes by stating that no other significant changes that would affect the investment recommendation process have occurred or are expected to occur in the near future.

According to CFA Institute Standards of Professional Conduct, which of the following best describes the actions Holly should take with regard to the desk pen and the concert tickets offered to him by the CEO of BlucNote? Holly:

OptionsMultipleChoice

Andrew Carson is an equity analyst employed at Lee, Vincent, and Associates, an investment research firm. In a conversation with his supervisor, Daniel Lau, Carson makes the following two statements about defined contribution plans.

Statement I: Employers often face onerous disclosure requirements.

Statement 2: Employers often bear all the investment risk.

Carson is responsible for following Samilski Enterprises (Samilski), a publicly traded firm that produces motorcycles and other mechanical parts. It operates exclusively in the United States. At the end of its 2009 fiscal year, Samilski's employee pension plan had a projected benefit obligation (PBO) of $320 million. Also, unrecognized prior service costs were $35 million, the fair value of plan assets was $316 million, and the unrecognized actuarial gain was $21 million.

Carson believes the rate of compensation increase will be 5% as opposed to 4% in the previous year, and the discount rate will be 7% as opposed to 8% in the previous year.

This past year, Samilski began using special purpose entities (SPEs) for various reasons. In preparation for analyzing the SPE disclosures in the footnotes to the financial statements, Carson prepares a memo on SPEs. In the memo, he correctly concludes that the company will be required under new accounting rules to classify them as variable interest entities (VIE) and consolidate the entities on the balance sheet rather than report them using the equity method as in the past.

Which of the following items, when recognized, will likely increase:

PBO? Pension expense?

OptionsMultipleChoice

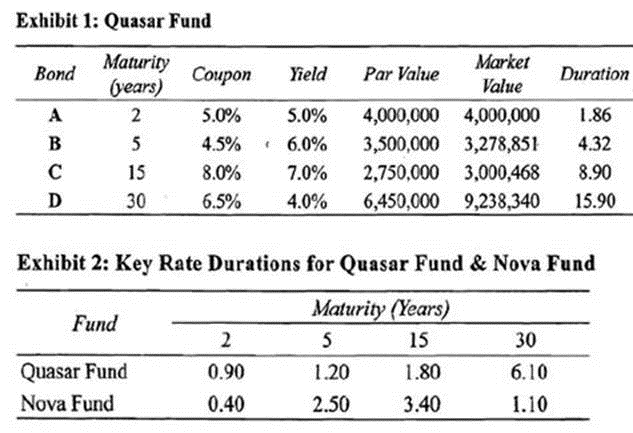

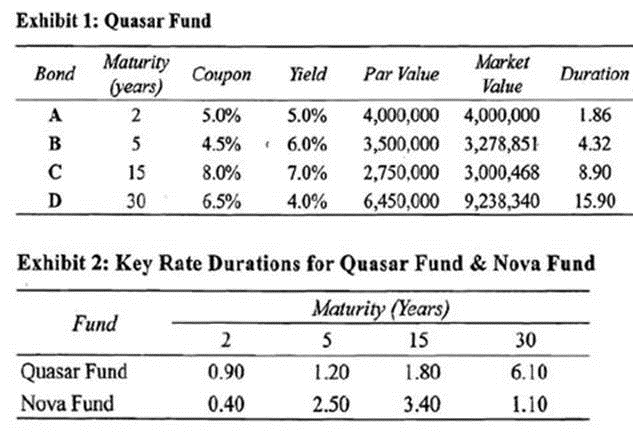

Martha Garret, CFA, manages fixed income portfolios for Jones Brothers, Inc. (JBI). JBI has been in the portfolio management business for over 23 years and provides investors with access to actively managed equity and fixed-income portfolios. All of JBI's fixed-income portfolios are constructed using U .S . debt instruments. Garret's primary portfolio responsibilities are the Quasar Fund and the Nova Fund, both of which are long fixed-income portfolios consisting of Treasury securities in all maturity ranges. The Quasar Fund holdings as of March 15 are provided in Exhibit 1. A comparison of key rate durations for the Quasar Fund and Nova Fund is provided in Exhibit 2.

Of particular importance to Garret and her colleagues is the degree of interest rate risk exposure unique to each portfolio under JBI's management. Driving the increased awareness of the portfolios' interest rate exposure is the double digit growth in assets under management that JBI's fixed-income portfolios have experienced in the last five years. Interest in the company's fixed-income portfolios continues to grow and as a result, all portfolio managers are required to attend weekly meetings to discuss key portfolio risk factors. At the last meeting, Miranda Walsh, a principal at JBI, made the following comments:

"The variance of daily interest rate changes has been trending higher over the last three months leading us to believe that a period of high volatility is approaching in the next twelve to eighteen months. However, the reliability is questionable since the volatility estimates were derived using an option pricing model, which assumes constant interest rates."

"Also, the Treasury spot rate curve currently has a similar shape to the yield curve on Treasury coupon securities, which, according to the market segmentation theory of interest rate term structure, indicates a relatively high level of demand from investors for intermediate term securities. Overzealous trading by investors unwilling to move into other maturity ranges may create mispricing and opportunities for arbitrage."

After the meeting, Walsh and JBI's other principals met to discuss a new international portfolio opportunity. At Walsh's suggestion, the principals selected Garret as the lead portfolio manager for the new fund, which will be titled the Atlantic Fund. One of the other portfolio managers, Greg Terry, CFA, suggested to Garret that she utilize the LIBOR swap curve as a benchmark for the Atlantic fund rather than using local government yield curves. Terry justifies his suggestion by claiming that "the lack of government regulation in the swap market makes swap rates and curves directly comparable between different countries despite fewer maturity points with which to construct the curve as compared to a government yield curve. Furthermore, credit risk in the swap curves of various countries is similar, thus avoiding the complications associated with different levels of sovereign risk embedded in government yield curves.'' Intrigued by the idea of using the swap curve, Garret has her assistant begin gathering a range of current and forward LIBOR rates.

Calculate the effect of a 75 basis point decrease in the 15-year interest rate and a 50 basis point increase in the 2-year interest rate on the value of the Nova Fund.

OptionsMultipleChoice

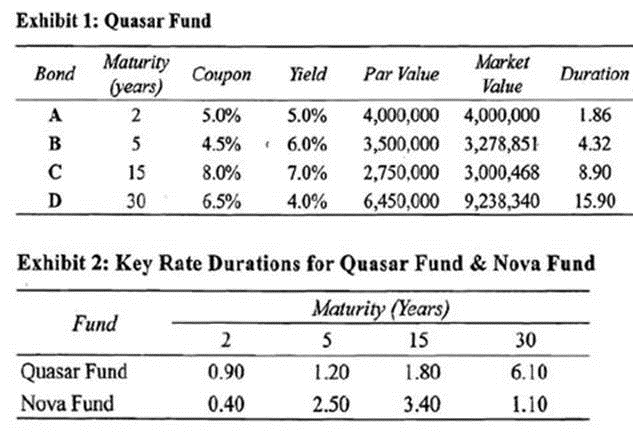

Martha Garret, CFA, manages fixed income portfolios for Jones Brothers, Inc. (JBI). JBI has been in the portfolio management business for over 23 years and provides investors with access to actively managed equity and fixed-income portfolios. All of JBI's fixed-income portfolios are constructed using U .S . debt instruments. Garret's primary portfolio responsibilities are the Quasar Fund and the Nova Fund, both of which are long fixed-income portfolios consisting of Treasury securities in all maturity ranges. The Quasar Fund holdings as of March 15 are provided in Exhibit 1. A comparison of key rate durations for the Quasar Fund and Nova Fund is provided in Exhibit 2.

Of particular importance to Garret and her colleagues is the degree of interest rate risk exposure unique to each portfolio under JBI's management. Driving the increased awareness of the portfolios' interest rate exposure is the double digit growth in assets under management that JBI's fixed-income portfolios have experienced in the last five years. Interest in the company's fixed-income portfolios continues to grow and as a result, all portfolio managers are required to attend weekly meetings to discuss key portfolio risk factors. At the last meeting, Miranda Walsh, a principal at JBI, made the following comments:

"The variance of daily interest rate changes has been trending higher over the last three months leading us to believe that a period of high volatility is approaching in the next twelve to eighteen months. However, the reliability is questionable since the volatility estimates were derived using an option pricing model, which assumes constant interest rates."

"Also, the Treasury spot rate curve currently has a similar shape to the yield curve on Treasury coupon securities, which, according to the market segmentation theory of interest rate term structure, indicates a relatively high level of demand from investors for intermediate term securities. Overzealous trading by investors unwilling to move into other maturity ranges may create mispricing and opportunities for arbitrage."

After the meeting, Walsh and JBI's other principals met to discuss a new international portfolio opportunity. At Walsh's suggestion, the principals selected Garret as the lead portfolio manager for the new fund, which will be titled the Atlantic Fund. One of the other portfolio managers, Greg Terry, CFA, suggested to Garret that she utilize the LIBOR swap curve as a benchmark for the Atlantic fund rather than using local government yield curves. Terry justifies his suggestion by claiming that "the lack of government regulation in the swap market makes swap rates and curves directly comparable between different countries despite fewer maturity points with which to construct the curve as compared to a government yield curve. Furthermore, credit risk in the swap curves of various countries is similar, thus avoiding the complications associated with different levels of sovereign risk embedded in government yield curves.'' Intrigued by the idea of using the swap curve, Garret has her assistant begin gathering a range of current and forward LIBOR rates.

Which of the following statements regarding the effects of interest rate changes on the Quasar Fund and Nova Fund is most accurate? The value of the:

OptionsMultipleChoice

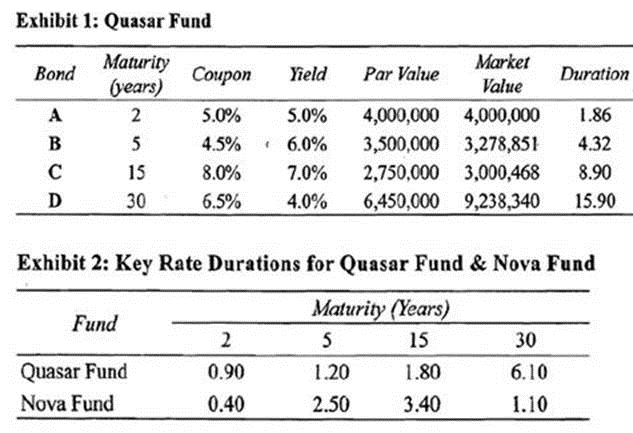

Martha Garret, CFA, manages fixed income portfolios for Jones Brothers, Inc. (JBI). JBI has been in the portfolio management business for over 23 years and provides investors with access to actively managed equity and fixed-income portfolios. All of JBI's fixed-income portfolios are constructed using U .S . debt instruments. Garret's primary portfolio responsibilities are the Quasar Fund and the Nova Fund, both of which are long fixed-income portfolios consisting of Treasury securities in all maturity ranges. The Quasar Fund holdings as of March 15 are provided in Exhibit 1. A comparison of key rate durations for the Quasar Fund and Nova Fund is provided in Exhibit 2.

Of particular importance to Garret and her colleagues is the degree of interest rate risk exposure unique to each portfolio under JBI's management. Driving the increased awareness of the portfolios' interest rate exposure is the double digit growth in assets under management that JBI's fixed-income portfolios have experienced in the last five years. Interest in the company's fixed-income portfolios continues to grow and as a result, all portfolio managers are required to attend weekly meetings to discuss key portfolio risk factors. At the last meeting, Miranda Walsh, a principal at JBI, made the following comments:

"The variance of daily interest rate changes has been trending higher over the last three months leading us to believe that a period of high volatility is approaching in the next twelve to eighteen months. However, the reliability is questionable since the volatility estimates were derived using an option pricing model, which assumes constant interest rates."

"Also, the Treasury spot rate curve currently has a similar shape to the yield curve on Treasury coupon securities, which, according to the market segmentation theory of interest rate term structure, indicates a relatively high level of demand from investors for intermediate term securities. Overzealous trading by investors unwilling to move into other maturity ranges may create mispricing and opportunities for arbitrage."

After the meeting, Walsh and JBI's other principals met to discuss a new international portfolio opportunity. At Walsh's suggestion, the principals selected Garret as the lead portfolio manager for the new fund, which will be titled the Atlantic Fund. One of the other portfolio managers, Greg Terry, CFA, suggested to Garret that she utilize the LIBOR swap curve as a benchmark for the Atlantic fund rather than using local government yield curves. Terry justifies his suggestion by claiming that "the lack of government regulation in the swap market makes swap rates and curves directly comparable between different countries despite fewer maturity points with which to construct the curve as compared to a government yield curve. Furthermore, credit risk in the swap curves of various countries is similar, thus avoiding the complications associated with different levels of sovereign risk embedded in government yield curves.'' Intrigued by the idea of using the swap curve, Garret has her assistant begin gathering a range of current and forward LIBOR rates.

Evaluate Walsh's comments regarding the method used to estimate the expected increase in interest rate volatility and the term structure of interest rates.

OptionsMultipleChoice

Martha Garret, CFA, manages fixed income portfolios for Jones Brothers, Inc. (JBI). JBI has been in the portfolio management business for over 23 years and provides investors with access to actively managed equity and fixed-income portfolios. All of JBI's fixed-income portfolios are constructed using U .S . debt instruments. Garret's primary portfolio responsibilities are the Quasar Fund and the Nova Fund, both of which are long fixed-income portfolios consisting of Treasury securities in all maturity ranges. The Quasar Fund holdings as of March 15 are provided in Exhibit 1. A comparison of key rate durations for the Quasar Fund and Nova Fund is provided in Exhibit 2.

Of particular importance to Garret and her colleagues is the degree of interest rate risk exposure unique to each portfolio under JBI's management. Driving the increased awareness of the portfolios' interest rate exposure is the double digit growth in assets under management that JBI's fixed-income portfolios have experienced in the last five years. Interest in the company's fixed-income portfolios continues to grow and as a result, all portfolio managers are required to attend weekly meetings to discuss key portfolio risk factors. At the last meeting, Miranda Walsh, a principal at JBI, made the following comments:

"The variance of daily interest rate changes has been trending higher over the last three months leading us to believe that a period of high volatility is approaching in the next twelve to eighteen months. However, the reliability is questionable since the volatility estimates were derived using an option pricing model, which assumes constant interest rates."

"Also, the Treasury spot rate curve currently has a similar shape to the yield curve on Treasury coupon securities, which, according to the market segmentation theory of interest rate term structure, indicates a relatively high level of demand from investors for intermediate term securities. Overzealous trading by investors unwilling to move into other maturity ranges may create mispricing and opportunities for arbitrage."

After the meeting, Walsh and JBI's other principals met to discuss a new international portfolio opportunity. At Walsh's suggestion, the principals selected Garret as the lead portfolio manager for the new fund, which will be titled the Atlantic Fund. One of the other portfolio managers, Greg Terry, CFA, suggested to Garret that she utilize the LIBOR swap curve as a benchmark for the Atlantic fund rather than using local government yield curves. Terry justifies his suggestion by claiming that "the lack of government regulation in the swap market makes swap rates and curves directly comparable between different countries despite fewer maturity points with which to construct the curve as compared to a government yield curve. Furthermore, credit risk in the swap curves of various countries is similar, thus avoiding the complications associated with different levels of sovereign risk embedded in government yield curves.'' Intrigued by the idea of using the swap curve, Garret has her assistant begin gathering a range of current and forward LIBOR rates.

Which of the following best evaluates Terry's justification for using the swap curve as the benchmark for the Atlantic Fund? Terry's justification is:

Options