Free Preparation Discussions

AICPA CPA-Regulation Exam Questions

- Topic 1: Review engagement and evaluate information

- Topic 2: Planning and measurement

- Topic 3: Accounting and reporting for governmental entities.

Free AICPA CPA-Regulation Exam Actual Questions

Note: Premium Questions for CPA-Regulation were last updated On Jul. 07, 2026 (see below)

John and Mary were divorced in 1991. The divorce decree provides that John pay alimony of $10,000 per year, to be reduced by 20% on their child's 18th birthday. During 1992, John paid $7,000 directly to Mary and $3,000 to Spring College for Mary's tuition. What amount of these payments should be reported as income in Mary's 1992 income tax return?

Choice 'b' is correct. Alimony would be income to Mary while child support would not. Funds qualify as child support only if 1) a specific amount is fixed or is contingent on the child's status (e.g., reaching a certain age), 2) it is paid solely for the support of minor children, and 3) it is payable by decree, instrument or agreement. The actual use of the funds is irrelevant to the issue. In this case, $2,000 (20% $10,000) qualifies as child support. The other $8,000 is alimony, which would be income to Mary.

Choice 'a' is incorrect. Take 80% of the $10,000 paid, not 80% of the $7,000 received by Mary.

Choice 'c' is incorrect. Only $8,000 would be alimony per the divorce decree (80% $10,000).

Choice 'd' is incorrect. The 20% reduction when the child turns 18 makes 20% of the $10,000 payment, or $2,000, child support, which is nontaxable to Mary.

The uniform capitalization method must be used by:

I Manufacturers of tangible personal property.

II Retailers of personal property with $2 million dollars in average annual gross receipts for the 3 preceding years.

Choice 'a' is correct. I only.

Rule: The uniform capitalization rules apply to the following:

1. Real or tangible personal property produced by the taxpayer for use in a trade or business.

2. Real or tangible personal property produced by the taxpayer for sale to customers.

3. Real or personal property acquired by the taxpayer for resale.

4. However, the uniform capitalization rules do not apply to property acquired for resale if the taxpayer's annual gross receipts for the preceding three tax years do not exceed $10,000,000 (not $2 million).

Elm Corp. is an accrual-basis calendar-year C corporation with 100,000 shares of voting common stock issued and outstanding as of December 28, 1996. On Friday, December 29, 1996, Hall surrendered 2,000 shares of Elm stock to Elm in exchange for $33,000 cash. Hall had no direct or indirect interest in Elm after the stock surrender. Additional information follows:

What amount of income did Hall recognize from the stock surrender?

Choice 'd' is correct. $17,000 capital gain.

Amount realized:

Choices 'a' and 'b' are incorrect. Dividends are distributions of earnings. These proceeds are from the sale of stock.

Choice 'c' is incorrect, per above. Accumulated earnings and profits do not effect the gain calculation, they only affect the taxability of dividends paid to shareholders.

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent.

Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040.

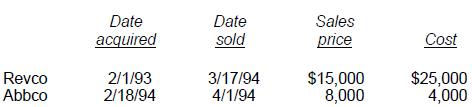

The Moores had no capital loss carryovers from prior years. During 1994, the Moores had the following stock transactions, which resulted in a net capital loss:

'J' is correct. $3,000. The capital loss on Revco ($10,000 loss) is added to the capital gain on Abbco ($4,000) to produce a net capital loss of ($6,000). The Moores can claim $3,000 of the loss on their 1994 income tax return and carry the balance forward to 1995.

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent.

Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040.

In 1992, Joan received an acre of land as an inter-vivos gift from her grandfather. At the time of the gift, the land had a fair market value of $50,000. The grandfather's adjusted basis was $60,000. Joan sold the land in 1994 to an unrelated third party for $56,000.

'A' is correct. $0. Property received by gift has two bases: one for computing gain and another for computing loss. Joan's basis for gain is the grandfather's adjusted basis ($60,000). Using this basis for gain, Joan has a loss of: $56,000 - $60,000 = ($4,000 loss). Joan's basis for loss is the fair market value of the property on the date of the gift ($50,000). Using this basis for loss, Joan has a gain of: $56,000 - $50,000 = $6,000 gain. In this unusual situation, Joan has neither a gain nor a loss, although the transaction must be reported.

- Select Question Types you want

- Set your Desired Pass Percentage

- Allocate Time (Hours : Minutes)

- Create Multiple Practice tests with Limited Questions

- Customer Support

Betty Evans

7 days agoMonica Mitchell

1 month agoEric Johnson

2 months agoJohn Lee

3 months agoRachel Reed

3 months agoStephanie King

2 months agoMonica Turner

2 months agoBrenda Peterson

2 months agoHeather Carter

3 months agoKanisha

3 months agoRosann

4 months agoYuriko

4 months agoFletcher

4 months agoBette

4 months agoStephane

5 months agoJames

5 months agoSherly

5 months agoJill

6 months agoChau

6 months agoKanisha

6 months agoRoxane

6 months agoFlorinda

7 months agoAlecia

7 months agoSherita

7 months agoOra

7 months agoTammy

8 months agoMari

8 months agoKris

8 months agoLili

8 months agoTricia

9 months agoAshley

9 months agoDick

9 months agoLettie

9 months agoBilly

10 months agoAlpha

10 months agoBarabara

10 months agoPenney

10 months agoTony

1 year agoBasilia

1 year agoLevi

1 year agoWava

1 year agoMaryann

1 year agoDaren

1 year agoKati

1 year agoEveline

1 year agoVannessa

1 year agoAudry

1 year agoJaclyn

1 year agoDaniela

1 year agoShawn

1 year agoRolf

1 year agoAngella

1 year agoJettie

1 year agoJulie

2 years agoAlfreda

2 years agoDetra

2 years agoBettye

2 years agoSage

2 years agoDortha

2 years agoAnnamaria

2 years agoAshley

2 years agoMatthew

2 years agoMiriam

2 years agoMarshall

2 years agoYuette

2 years agoHubert

2 years agoTiara

2 years agoBarrie

2 years agoGianna

2 years agoEnola

2 years agoElina

2 years agoCarman

2 years agoErasmo

2 years agoGlory

2 years agoGwenn

2 years agoDaren

2 years agoCraig

2 years agoLisbeth

2 years ago