Free Preparation Discussions

CFA Institute CFA-Level-II Exam - Topic 3 Question 70 Discussion

Topic #: 3

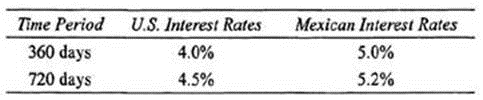

Rock Torrey, an analyst for International Retailers Incorporated (IRI), has been asked to evaluate the firm's swap transactions in general, as well as a 2-year fixed for fixed currency swap involving the U .S . dollar and the Mexican peso in particular. The dollar is Torrey's domestic currency, and the exchange rate as of June 1,2009, was $0.0893 per peso. The swap calls for annua! payments and exchange of notional principal at the beginning and end of the swap term and has a notional principal of $100 million. The counterparty to the swap is GHS Bank, a large full-service bank in Mexico.

The current term structure of interest rates for both countries is given in the following table:

Torrey believes the swap will help his firm effectively mitigate its foreign currency exposure in Mexico, which sterns mainly from shopping centers in high-end resorts located along the eastern coastline. Having made this conclusion, Torrey begins writing his report for the management of IRI. In addition to the terms of the swap, Torrey includes the following information in the report:

* Implicit in the currency swap under consideration is a swap spread of 75 basis points over 2-year U .S . Treasury securities. This represents a 10 basis point narrowing of the spread as compared to this time last year. Thus, we can assume that the credit risk of the global credit market has decreased. Unfortunately, the decline provides no insight into the credit risk of the individual currency swap with GHS Bank, which could have increased.

* In order to decrease the counterparty default risk on the currency swap, we will need to utilize credit derivatives between the beginning and midpoint of the swap's life when this particular risk is at its highest. This is a significantly different strategy than we normally use with interest rate swaps. For interest rate swaps, counterparty default risk peaks at the middle of the swap's life, at which point we utilize credit derivative CQuntermeasures to offset the risk.

* Because currency swaps almost always include netting agreements and interest rate swaps can be structured to include mark-to-market agreements, we can significantly reduce the credit risk of these swap instruments by negotiating swap contracts that include these respective features. When negotiating these features is not possible, credit risk can be reduced by using off-market swaps that do not require an initial payment from IRI.

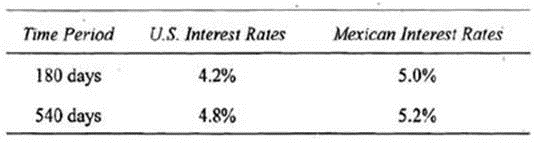

Six months have passed (180 days) since Torrey issued his report to IRI's management team, and the current exchange rate is now $0,085 per peso. The new term structure of interest rates is as follows:

Which of the following statements correctly assesses the excerpt from Torrey's report regarding the swap spread on the currency swap under consideration? Torrey's statement is:

The swap spread is derived from the term structure of interest rates used to price the cash flows of the swap. These rates do not reflect the credit risk of the counterparties. They reflect the credit risk in the overall global economy because they reflect the credit spread of the reference rate used to calculate the fixed-rate and expected floating-rate payments. (Study Session 17, LOS 61.})

Portia

8 months agoJunita

8 months agoCaren

8 months agoMillie

9 months agoHerman

9 months agoRessie

9 months agoYvonne

9 months agoLoren

9 months agoLaurel

9 months agoNettie

9 months agoKarina

9 months agoMoon

9 months agoKimberlie

9 months agoYan

9 months ago