Free Preparation Discussions

CIMAPRO19-P01-1 Exam Questions

- Topic 1: Determine causality in cost function estimates and impact on budgets/ Identify inventory costs and period costs

- Topic 2: Determine the activity that causes the change in cost/ Understand the difference between variable costs and fixed costs

- Topic 3: Understand relevant cash flows and their use in pricing decisions/ Calculate the costs for products or services using activity-based costing

- Topic 4: Calculate the breakeven point and output level required to meet income targets/ Understand costing and the different reasons for calculating costs

- Topic 5: Understand the impact of individuals’ risk attitudes on decision-making in the short term/ Understand the difference between direct costs and indirect costs

- Topic 6: Calculate revenue and cost estimates using quantitative analyses/ Calculate and interpret overall flexed budget variances

- Topic 7: Understand relevant cash flows and non-financial factors and how it affects make or buy decisions/ Understand the strategic implications of short-term decision-making

- Topic 8: Understand how budgets can help energize and motive individuals and teams/ Recognise how management accountants help make tactical business decisions

- Topic 9: Calculate subdivision of total usage/efficiency variances into mix and yield variances/ Use material, labour, variable overhead, fixed overhead and sales variances

- Topic 10: Establish manufacturing standards for material, labour, variable overhead and fixed overhead/ Understand the difference between financial accounting and cost accounting

Free CIMA CIMAPRO19-P01-1 Exam Actual Questions

Note: Premium Questions for CIMAPRO19-P01-1 were last updated On Jul. 11, 2026 (see below)

Company LGF seeks to maximize profits and has a 'risk seeker' attitude when making decisions. The company has to choose between mutually exclusive projects. A range of possible profit outcomes has been estimated for each project along with their associated probabilities.

Company LGF would choose the project with the:

A manager must select one of three projects, W, X or Y.

The following payoff table has been prepared to show the outcomes in $000 at three possible levels of demand:

The manager is now preparing a regret matrix.

What figure (in $000) will be shown for Project Y in the regret matrix if the average demand arises?

Explain the advantages of management participation in budget setting and the potential problems that may arise in the use of the resulting budget as a control mechanism.

Select all the correct answers.

References:

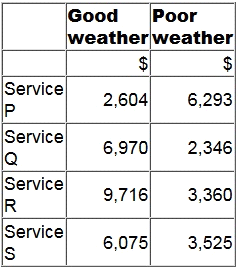

A manager is deciding which one of four services to provide next period.

The contribution earned by each service will depend on the weather conditions as follows.

Using the maximin criterion, which service will the manager provide?

- Select Question Types you want

- Set your Desired Pass Percentage

- Allocate Time (Hours : Minutes)

- Create Multiple Practice tests with Limited Questions

- Customer Support

Eric Torres

8 days agoMonica Rodriguez

15 days agoLisa Morgan

1 month agoRebecca Wright

2 months agoRachel Walker

2 months agoSarah Nguyen

3 months agoJustin Ramirez

3 months agoKimberly Nguyen

3 months agoAdam Roberts

2 months agoChristopher Taylor

3 months agoJennifer Scott

2 months agoSheridan

3 months agoWillard

4 months agoAdelina

4 months agoRex

4 months agoIsabella

4 months agoNada

5 months agoLemuel

5 months agoAmalia

5 months agoReena

6 months agoLashandra

6 months agoErnest

6 months agoLatanya

6 months agoStephane

7 months agoDong

7 months agoTerry

7 months agoMatilda

7 months agoCecilia

8 months agoAllene

8 months agoDomonique

8 months agoAnnett

8 months agoShawnta

9 months agoCecily

9 months agoStevie

9 months agoLouvenia

9 months agoKasandra

10 months agoLinn

10 months agoKing

10 months agoBonita

10 months agoDell

1 year agoAlesia

1 year agoAshanti

1 year agoAnglea

1 year agoMattie

1 year agoTrinidad

1 year agoBen

1 year agoVernice

2 years agoAdelle

2 years agoDawne

2 years agoCrissy

2 years agoGeraldo

2 years agoIvan

2 years agoLina

2 years agoTomoko

2 years agoLorrie

2 years agoKristal

2 years agoRikki

2 years agoAliza

2 years agoLarae

2 years agoGarry

2 years agoPamella

2 years agoDusti

2 years agoCecily

2 years ago