Deal of The Day! Hurry Up, Grab the Special Discount - Save 25% - Ends In 00:00:00 Coupon code: SAVE25

Free Preparation Discussions

AAFM GLO_CWM_LVL_1 Exam - Topic 2 Question 24 Discussion

Actual exam question for

AAFM's

GLO_CWM_LVL_1 exam

Question #: 24

Topic #: 2

[All GLO_CWM_LVL_1 Questions]

Topic #: 2

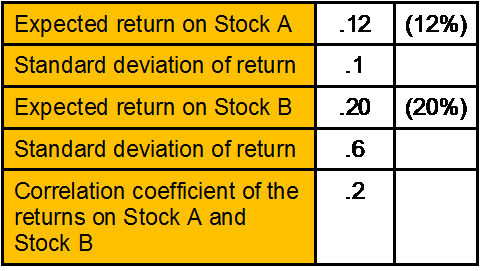

Given the following information:

What is the expected return and standard deviation of the portfolio if 50% of funds invested in each stock? What would be the impact if the correlation coefficient were 0.6 instead of 0.2?

Suggested Answer:

C

Chau

7 months agoCorrie

8 months agoAdria

8 months agoMaryanne

8 months agoMozell

8 months agoAllene

8 months agoAvery

9 months agoDianne

9 months agoDianne

9 months agoDianne

9 months agoDianne

9 months agoQuentin

9 months agoKasandra

10 months agoMarshall

10 months agoDana

10 months ago